September is National PACE month, which provides an opportunity to celebrate and focus on the innovations of the Program of All-Inclusive Care for the Elderly (PACE) in meeting the many challenges of supporting staff and participants through the COVID-19 pandemic and looking ahead to new opportunities in the coming years. The past couple of years have been difficult for senior living and services providers. Due to the COVID-19 pandemic, many organizations struggled to maintain census. As we begin to slowly move towards a post-COVID environment, senior living and providers are beginning to recoup census. In this post, we will explore how PACE continued to expand during COVID-19 and how PACE will see significant growth over the next few years as the demand for senior services returns to pre-COVID-19 levels.

PACE Philosophy and New 2022 Programs

PACE centers on the belief that it is better for the well-being of seniors with chronic care needs, and their families, to be served in the community whenever possible. By providing or coordinating all needed medical and supportive services through an interdisciplinary team (IDT), PACE programs are able to provide the entire continuum of care and services to older adults with chronic care needs, while enabling them to maintain independence in their homes for as long as possible.

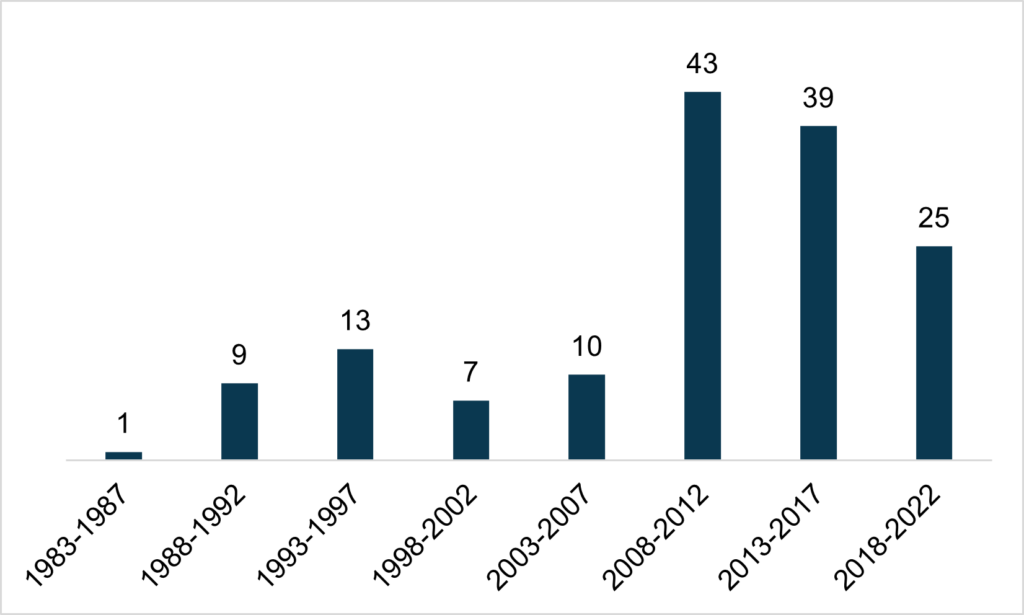

The number of new PACE providers grew by six programs in 2020, six in 2021, and five so far in 2022. It typically takes approximately 18–24 months to start a program. Needless to say, no provider that opened in 2020 or later opened in ideal circumstances.

Figure 1 shows the number of current PACE providers by time frame of opening.

Figure 1: PACE Programs by Time Frame Opened

Source: National PACE Association (NPA)

Source: National PACE Association (NPA)

Since 2018, there has been an average of five new programs opened each year. Over the past 10 years, there has been an average of 6.4 new programs opened per year, putting 2020 and 2021 at average years, despite the expanded difficulties of opening during a pandemic. Five programs have opened in 2022 with a few more months to go indicating the growth of new programs has remained stable.

Dual-Eligible Enrollment Growth

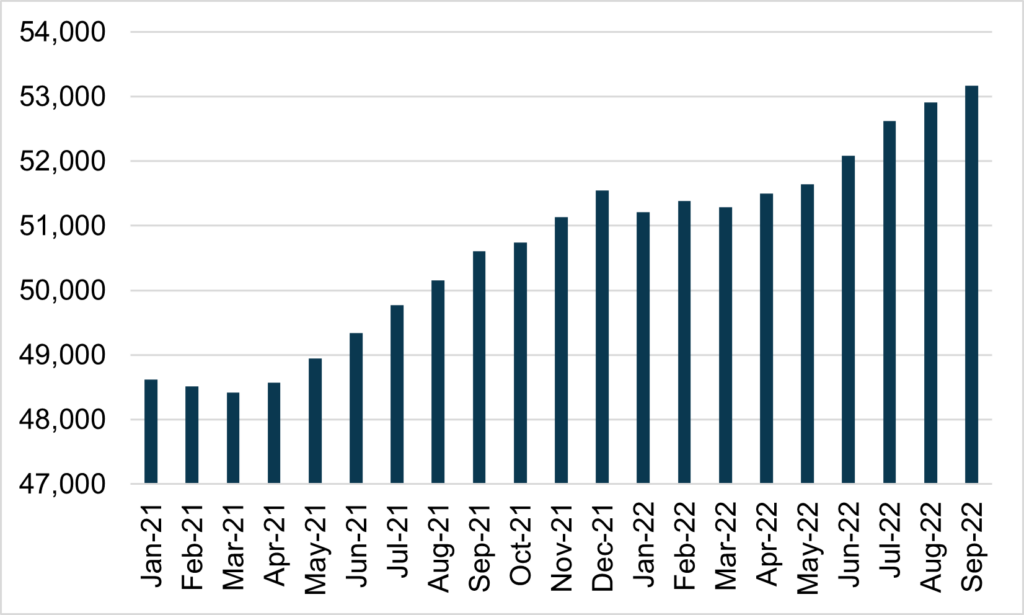

All senior services providers were impacted by COVID-19 in 2020 and 2021. Understandably, most providers experienced a decline in census and have struggled to regain pre-COVID-19 levels. One exception to the decline in census is PACE. Even with increased challenges in service delivery, dual-eligible enrollment increased by 6.0 percent from January 2021 through December 2021. Dual-eligible enrollment has increased by 3.8 percent from January 2022 through September 2022. Figure 2 shows the month-to-month dual-eligible enrollment.

Figure 2: Dual-Eligible PACE Enrollment in January 2021 – September 2022

Source: Centers for Medicare & Medicaid Services (CMS)

Source: Centers for Medicare & Medicaid Services (CMS)

In both years, dual-eligible enrollment had a small decline sometime during the first quarter, but experienced consistent growth the remainder of the year.

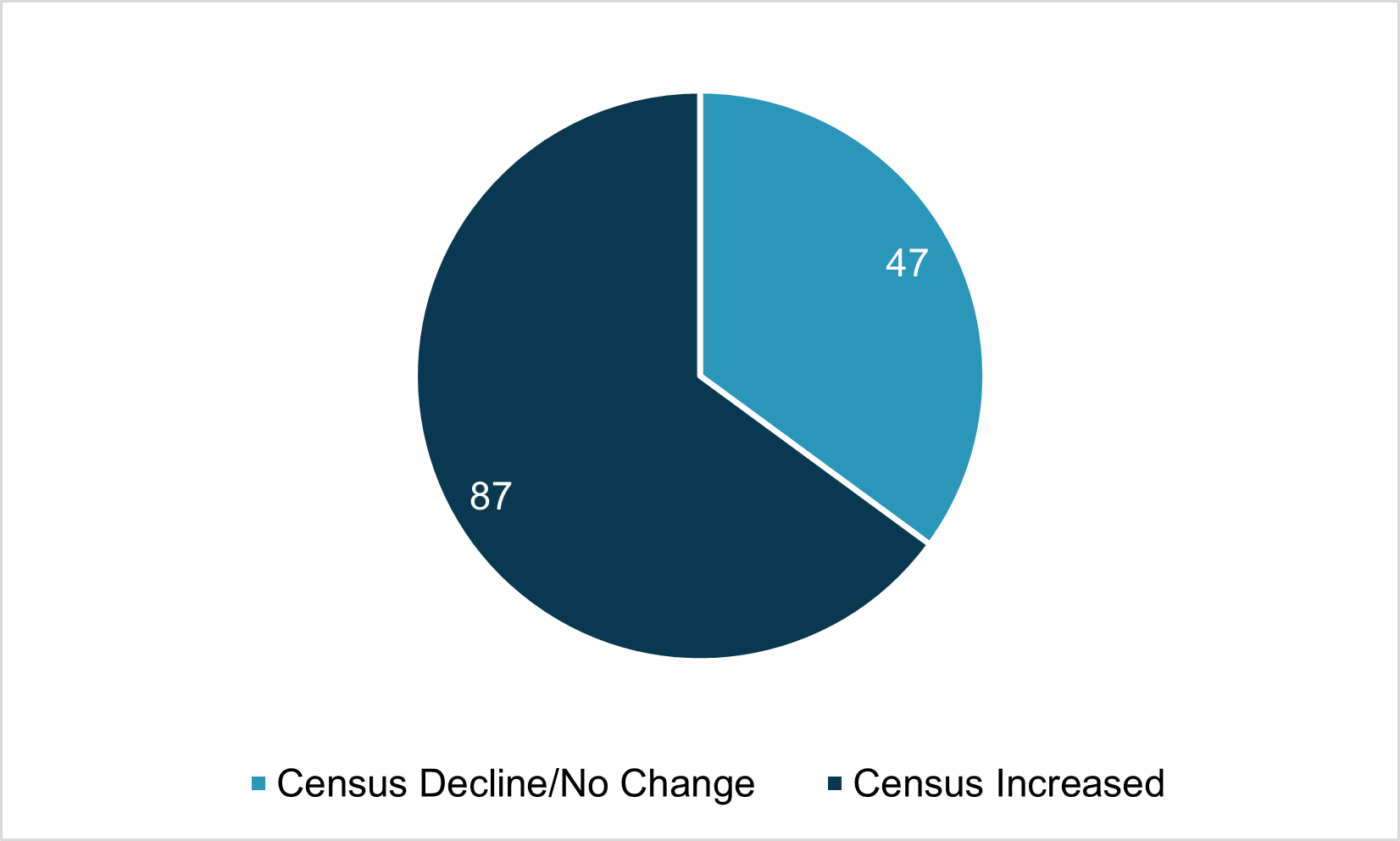

Some of the PACE dual-eligible enrollment growth is attributed to the addition of six new programs in 2021 and five new programs so far in 2022. However, that only accounts for a small percentage of the overall increase. Figure 3 shows how the 134 programs that were in operation in January 2021 have fared since.

Figure 3: Dual-Eligible Enrollment Change in Programs Open All 21 Months

Source: CMS

Source: CMS

As shown on Figure 3, for programs that were operating in January 2021, most have increased in census.

- Of the 47 programs that experienced a decline in census, the median decline was 19 enrollees.

- Of the 87 programs that experienced an increase in census, the median increase was 37 enrollees.

- Overall, the 134 programs that were open on January 1, 2021, experienced a cumulative growth of 5.5 percent through December 2021.

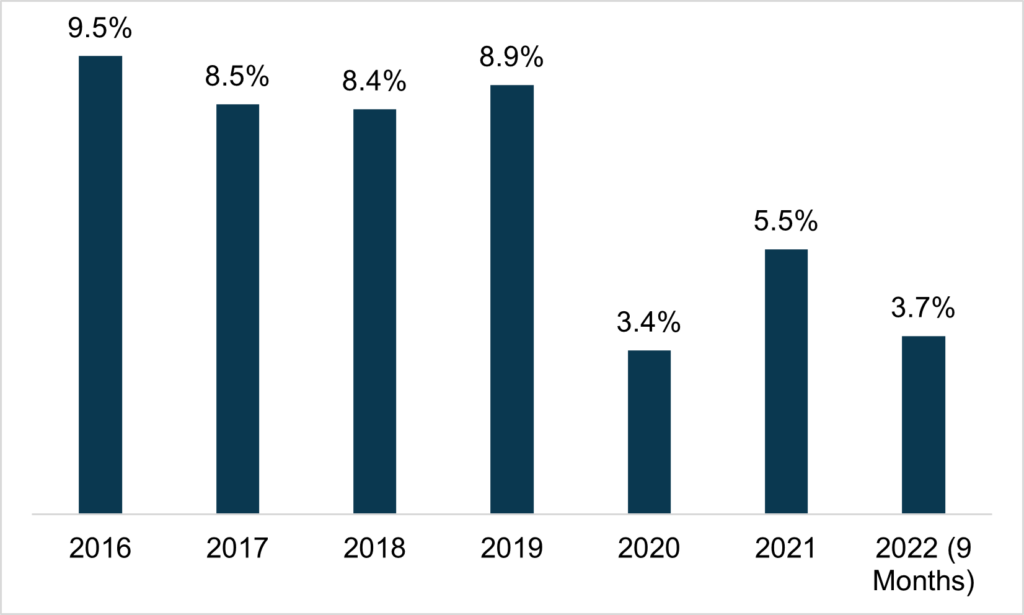

Figure 4 shows annual program growth for programs that were open for the full 12 months during prior years.

Figure 4: Annual Growth of Programs Open Full Year 2016–2022

Source: CMS

Source: CMS

As shown on Figure 4, if we eliminate any dual-eligible growth resulting from the opening of new programs, PACE programs experienced a cumulative annual growth of between 8.4 percent and 9.5 percent between 2016 and 2019. Although 2020 saw a significant decline in growth from prior years, PACE still experienced overall growth during the pandemic. Growth in 2021 did not quite hit pre-COVID-19 levels but was higher than 2020. Growth in 2022 has exceeded 2020 levels and with one full quarter remaining should reach similar levels as 2021.

Why Does PACE Continue to Grow?

PACE is an at-risk model, which means the program is responsible for directly providing or coordinating and paying for all of its participants’ care needs. Unlike traditional Medicare Fee-for-Service (MFFS), PACE programs have flexibility in how capitation dollars are used to provide the services their participants need. When PACE centers were closed or limited to only necessary clinic visits, programs had to be creative in developing new ways to care for participants. These creative measures included redefining staff responsibilities, utilizing telehealth technology, and shifting to delivering care and meals in the home rather than in the PACE center.

If there is a silver lining for PACE programs during this pandemic, it is that the ingenuity displayed by PACE leaders may reveal new approaches to the PACE model of care that will continue to evolve after the COVID-19 pandemic runs its course.

Future Growth of PACE

In response to the challenges of operating in a COVID-19 environment, many states have encouraged the expansion of PACE. Existing PACE states such as Louisiana, Maryland, New Jersey, North Dakota and Virginia released Requests for Proposals (RFP) for PACE expansion, while the District of Columbia and Illinois released RFPs to open their first providers in the near future. Kentucky and Missouri recently opened programs increasing the number of states to 32 that have an operational PACE program. The increased federal funding for Medicaid home and community based services as part of the American Rescue Plan signed into law in March 2021 has caused many other states to consider investing in PACE development or expansion.

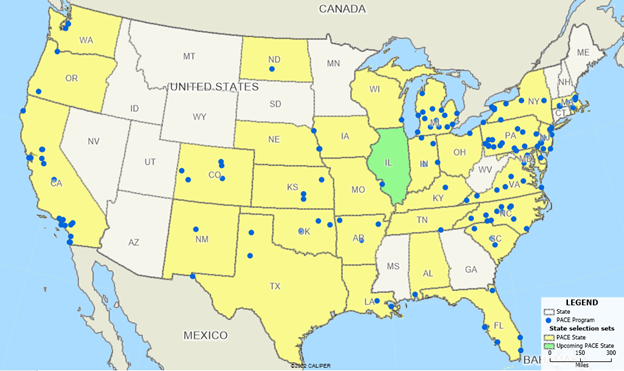

COVID-19 has highlighted the capabilities of the PACE model, and interest from organizations and financial investors in sponsoring PACE has accelerated, which is an indication that significant growth in new PACE plans is coming within the next few years. Figure 5 shows the number of programs operational as of September 2022.

Figure 5: PACE States and Provider Locations as of September 1, 2022

Source: National PACE Association

Source: National PACE Association

For More Information

As a National PACE Association Technical Assistance Center, Health Dimensions Group (HDG) has successfully assisted many organizations with PACE market and financial feasibility studies, program development and implementation support, and operational improvement. If you would like to learn more about how HDG can assist you in exploring PACE as a solution in today’s challenging health care environment, please contact us at 763.537.5700 or info@hdgi1.com and visit our website.